First, the life cycle and industry scale of the industry

(1) Development history and current situation of China's medical device manufacturing industry

The demand for medical device market in China has continued to grow in recent years, and it is expected that there will still be room for growth in the future. In recent years, China's medical device industry development and investment are more active, the national strategic emerging industry policy guidance and the upgrading of domestic medical and health institutions' equipment will make the future medical device consumer market continue to grow.

In the past 13 years, the sales volume of China's medical device market has increased from 17.9 billion yuan in 2001 to 212 billion yuan in 2013. Excluding the impact of price factors, it has increased by 10.84 times in 13 years. According to the sample survey of the Medical Devices Branch of China Pharmaceuticals (17.33, 1.580, 10.03%), the national medical device sales volume in 2014 was about 255.6 billion yuan, an increase of 43.6 billion yuan over the 2013 revenue of 212 billion yuan. The growth rate is 20.57%.

The global consumption ratio of medicines and medical devices is about 1:0.7. The developed countries such as Europe, America and Japan have reached 1:1.02. The global medical device market has occupied 42% of the total size of the international pharmaceutical market, and it has expanded. In 2014, the total size of China's medical device market was about 255.6 billion yuan. The total size of the pharmaceutical market is estimated at 1,322.6 billion yuan. The ratio of medicines to medical consumption is 1:0.19. The ratio of medicines to medical consumption in 2013 was 1:0.2. It is expected that there will still be room for growth in the medical device market in the future.

The number of medical device manufacturing enterprises in China has increased year by year: in 2010, there were 14,337, including 4015 medical device manufacturers, 7906 medical device manufacturers, and 2,416 medical device manufacturers, and national and provincial key enterprises. 1863 homes. As of the end of November 2012, the number of medical device manufacturers nationwide has rapidly increased to more than 16,000. State-owned enterprises, foreign-funded enterprises and joint ventures and private enterprises accounted for 3%, 37% and 60% respectively. Among them, there are more than 200 enterprises with an output value of over 100 million yuan; less than 20 enterprises with an output value of over 1 billion yuan, and foreign-invested enterprises and joint-venture enterprises account for the vast majority. According to statistics in 2011, foreign and Hong Kong, Macao and Taiwan investment enterprises constitute the main force of China's medical device industry, and its assets account for 43% of the total assets of China's medical device industry.

There are many domestic medical device manufacturers, and the market concentration is low. According to geographical distribution, the domestic brand medical device industry in the east and south coastal areas represented by Shanghai and Shenzhen is characterized by “multiple, small, high and weakâ€: First, there are many production enterprises. By the end of 2013, there were 15,698 medical device manufacturers in China. The second is the small scale of enterprises. In 2013, the total output value of the medical device industry market was 221 billion yuan, and the average output value of each enterprise was about 1,350. 10,000 yuan, an increase of 1.5 million yuan and 12.5% ​​over the previous year; the third is high product concentration, more than 3,500 types of medical device products, an average of more than 10 registration certificates for each product; the fourth is relatively internationally renowned Brand, technical level is relatively weak. In recent years, with the continuous improvement of China's technical level and the continuous improvement of the manufacturing capabilities of precision manufacturing and mechatronics equipment, China's medical device industry has developed rapidly. From 2000 to 2012, the size of the medical device industry increased by an average of more than 20% per year. In 2012, China's medical device market has exceeded 150 billion yuan, and China has become one of Asia's top medical device manufacturers and one of the world's top ten emerging markets for medical devices. In the next few years, China will surpass Japan to become the world's second largest medical device market.

In general, medical device listed companies have certain scale advantages, but the industrial concentration is still not enough: In 2014, the annual sales revenue of 20 listed companies engaged in medical device production and operation was estimated at 37.2 billion yuan, accounting for the total sales of the industry. 14.55% of the amount. From the perspective of geographical distribution, China's medical device industry is concentrated in the eastern and southern coastal areas. The Yangtze River Delta region, represented by Shanghai and Jiangsu, and the Bohai Bay region, represented by Beijing, are mainly attracting investment and forming a dominant industrial cluster with foreign-funded enterprises as the main body. In the Yangtze River Delta, products such as disposable injection and infusion sets are dominant in the country; CT machines represented by General Electric Company in Beijing have an absolute advantage; Shenzhen's medical device industry has grown from scratch, in just over 10 years. It has developed into an important manufacturing and processing base for China's high-end medical device industry. Medical imaging diagnostic equipment, patient monitors and other products also have a place in the international market, and the development momentum is strong.

(II) Space for development of industrial enterprises

According to the 2011 China Medical Device Industry Analysis and Development Forecast Report released by Shangpu Consulting, it is estimated that by 2015, the entire medical instrument and equipment market in China is expected to be nearly 340 billion yuan. At present, medical devices in the world account for 42% of the total size of the pharmaceutical market, while China's medical devices account for 14% of the total size of the pharmaceutical market, and the potential for market development is huge. According to the statistics of the Medical Devices Branch of the China Pharmaceutical Materials Association, as of December 2013, there were 15,700 enterprises holding medical device production licenses in China, including more than 35 medical devices listed at home and abroad. There were 93,592 types of medical devices that obtained medical device registration certificates in China, which were basically the same as the same period of last year, and 34,655 imported medical devices that obtained medical device registration certificates.

China has a registration system for medical devices, and the 2013 “drug supervision statistics†announced by the State Food and Drug Administration in November 2014. The number of re-registration of Class I and Class II medical devices increased significantly in the same year. Among them, the number of Class I re-registrations was 3,738, an increase of 36.47% compared with 2,739 in the previous year; the number of Class II re-registrations reached 5,801, an increase of 75.79 over the previous year's 3,300. %.

The policy orientation of promoting the development of digital diagnosis and treatment equipment and localization in China is very clear. According to the "12th Five-Year Plan for National Independent Innovation Capacity Building" issued by the State Council, the "Twelfth Five-Year National Strategic Emerging Industry Development Plan" issued by the Ministry of Industry and Information Technology, and the "Twelfth Five-Year Plan" for the Pharmaceutical Industry "The National "Twelfth Five-Year" Science and Technology Development Plan issued by the Ministry of Science and Technology, advanced medical equipment is an important industry related to the national economy and the people's livelihood, and is a key area of ​​strategic emerging industries that China vigorously develops and cultivates." During the Five-Year Plan period, China vigorously promoted the development of core components of medical imaging equipment, the development of key technologies, the development of high-end products, and the cultivation of key enterprises with strong independent innovation capabilities, improved the localization level of equipment, and improved the internationalization of China's medical device industry. Competitiveness. The company's various products are key development products.

Since 2014, the relevant state regulatory authorities have taken active measures to create a good development environment for the medical device industry: In 2014, the State Food and Drug Administration carried out a five-month “five rectification†special action, focusing on rectification. Five kinds of behaviors such as false registration of medical devices, illegal production, illegal operation, exaggeration of publicity, and use of unlicensed products have effectively regulated the market and contributed to the healthy development of the medical device industry. In March 2015, the Ministry of Science and Technology issued the digital diagnosis and treatment. The special equipment implementation plan (draft for comments), from 2015 to 2020, the main tasks of the development of the medical device industry are major equipment R&D, cutting-edge and common technology innovation, application solution research, application demonstration and evaluation research. After the “Twelfth Five-Year Plan†period of promotion and localization of industrial policy guidance and preparation, China will further increase the policy and investment of the digital diagnosis and treatment equipment industry in the future. During the “13th Five-Year Plan†period, the digital diagnosis and treatment equipment industry will achieve breakthroughs. Harvest, the future domestic digital diagnosis and treatment equipment will continue to develop at a high speed.

The medical imaging diagnostic equipment belongs to the middle and high-end medical equipment, which provides important guarantee for clinical diagnosis and treatment, and also provides an important platform for clinical scientific research. Commonly used medical imaging diagnostic equipment includes: X-ray machine, magnetic resonance imaging (MRI) equipment, Computed tomography (CT) equipment, etc.

2014 is an important year for the domestic medical imaging diagnostic equipment industry. Strong support from the national strategic level and the introduction of a series of new policies to promote domestic hospitals to replace imported equipment with domestically produced equipment, coupled with the accumulation of their own technology, talents and funds, domestic medical imaging diagnostic equipment companies are facing major development opportunities. It is expected that the process of localization of medical imaging diagnostic equipment will accelerate in the next few years, driving the rapid expansion of the domestic enterprise market.

Second, the industry competition pattern and industry barriers

(1) Industry competition pattern

According to the scale of operation and market share, the medical imaging diagnostic equipment manufacturing enterprises in the domestic market can be basically divided into three echelons, and the company is located in the second echelon. The first echelon is a multinational medical device company, including Philips, General Electric, Siemens, etc.; these companies have high software product and hardware equipment research and development, integration and sales capabilities, in addition to covering the main medical imaging diagnostic equipment, There are also many achievements in other types of medical device products. At present, the first echelon of multinational medical device companies occupy a high market in China's medical imaging diagnostic equipment.

The second echelon is the domestic excellent medical device companies such as Lanyun, Anjian Technology, Wandong Medical, Yuyue, Mindray Medical, New Huangpu (12.30, -1.370, -10.02%) and Lian Ying Medical. Brands and technologies are becoming more and more mature. The quality and performance of products can be compared with imported equipment. It is welcomed by more and more medical units with high cost performance and excellent after-sales service. They are the main competitors in the industry, and products are shifting from analog to digital. Our company is a digital product, and its comprehensive competitive strength ranks eighth in the catalogue of excellent domestic equipment.

The third echelon is mainly for small-scale medical device manufacturers with weak technical capabilities, low-end products and weak competitiveness.

(2) Industry entry barriers

The new entry enterprises in the medical device industry must achieve the scale and compete with existing enterprises. The following barriers exist:

1. Access barriers

Disposable medical device products cover Class I, Class II and Class III medical devices. The State Drug Administration Department implements strict medical device manufacturing enterprise licenses and product registration systems. New enterprises entering the industry need to pass the provincial drug regulatory department's review. In addition, the medical device manufacturing enterprise license and the medical device business enterprise license can be operated; in addition, the production enterprises in the industry must obtain the product registration certificate before the production and sales of the corresponding medical device products. Medical device manufacturers have strict audit requirements. Enterprises engaged in the production of Class II and Class III medical devices should have production equipment, sites and environments that are compatible with production requirements. The production, quality and technical leaders must have qualified professional qualifications. In terms of medical device registration, enterprises applying for registration of a class of medical devices need to have qualified quality management capabilities and corresponding resource conditions, and should provide a full performance test report for products, and enterprises applying for registration of Class II and Class III medical devices need Provide product technical reports, safety risk analysis reports, product performance self-test reports, clinical trial data, and product registration test reports issued by medical device testing organizations, etc., in the product trial production, registration inspection, clinical trials, registration declarations, etc. Strict standards and management regulations.

Enterprises can only engage in the production of medical devices under the premise of meeting the requirements of production environment, personnel quality, equipment configuration, etc., and the sales of all kinds of products need to complete a series of testing, analysis, clinical trials, and through the registration of products. Conducting, there are higher obstacles for newly entered companies.

2. Technical barriers

The medical device industry is a multi-disciplinary, knowledge-intensive, capital-intensive high-tech industry. The industry products are high-tech products that integrate medical, biomechanical, medical materials, and mechanical manufacturing. The accumulation of product know-how and the cultivation of research and development capabilities are a long-term process, and the general enterprises cannot be formed quickly in a short period of time. At the same time, the industry has extremely high requirements for the production environment, product manufacturing process and manufacturing equipment. The production and processing technology will directly determine the performance and use effect of the product, directly affecting the success rate of the operation. For most users, the main production equipment of the product is tailored according to its own production process, and is continuously optimized and improved in the long-term production process. It is difficult for companies that lack the required process equipment and lack of long-term process technology to produce qualified products with stable quality.

3. Market channel barriers

The establishment of a nationwide sales network and after-sales service system requires a large amount of capital investment, and the maintenance of the sales and after-sales service network requires a large number of high-margin space products as support; the conditions of the bidding project of the medical and health system are generally set high, and it takes many years to be good. Business performance and product quality as well as a comprehensive after-sales service network make it difficult for new entrants to enter the tendering market. Due to the wide geographical coverage, high professionalism, and scattered customers, the sales of medical devices generally use the “distribution-oriented, direct sales supplement†business model to sell to end users.

In addition to the need to have certain financial strength and marketing capabilities, dealers need to be able to provide professional services to end users, and help physicians coordinate and solve problems encountered in use. These dealers have basically entered the enterprise that is currently entering. Long-term and stable cooperation has been carried out, and it is difficult for new companies entering the industry to find a suitable dealer team in a short period of time.

In addition, the construction of a sound marketing network system requires not only a large amount of upfront capital investment, but also a long-term accumulation of deep understanding of the market and forward-looking grasp, as well as the brand effect of continuously creating value for customers. New entrants cannot be in a short time. Cultivate strong marketing channels.

4. Talent barriers

The medical device industry is a special high-tech industry. Medical device products integrate new technologies in various disciplines such as medicine, electronics, and automation control. Enterprises lacking in technology and research and development capabilities are difficult to enter. Core technical talents need to have comprehensive knowledge of medicine, electronics, automation control, etc., and must have many years of practical experience in the same industry; sales personnel need to have knowledge of marketing and product performance, use, etc.; these talents are difficult to cultivate in a short period of time.

5. Financial barriers

The medical device industry is a high-input industry. Without a certain amount of capital investment for product research and development and the establishment of sales and service networks, it is difficult for enterprises to survive in the market.

6, brand barriers

Medical devices are related to the life and health of users. Customers pay special attention to brands when they choose products. The brand effect accumulated by quality products for many years is an insurmountable obstacle for new entrants in the short term.

Third, the relationship between the industry and the industry upstream and downstream

The medical device industry's technological progress, enterprise growth and market expansion are closely related to the upstream and downstream industries. Medical device products have high requirements on the quality of raw materials, and the variety of products is complex. The upstream of the medical device industry is materials, electronics, machinery, non-ferrous metals (3978.04, -24.420, -5.74%) and other industries. The advancement of science and technology in the upstream industry will directly affect The technical direction of medical devices, such as the upstream manufacturing and manufacturing capabilities, determines the quality, technical level and cost of raw materials or semi-finished products.

The downstream of the medical device industry is mainly the final consumer. The products are directly used by consumers through hospitals and other medical institutions. The consumer demand and consumption capacity determine the size of the market, which affects and determines the market prospects and economic benefits of medical device products. .

Fourth, the state's regulatory system and policy for the industry

1. Industry authorities, regulatory systems and industry policies

(1) Industry authorities and functions

The competent authority of China's medical device industry is the State Food and Drug Administration. Its functions include: draft laws and regulations responsible for medical device supervision and management, formulating policy plans, formulating departmental regulations, organizing implementation, supervision and inspection; responsible for organizing the formulation and publication of medical treatment. Equipment standards, classification management systems, and medical device development, production, management, use quality management practices and supervision and implementation; responsible for medical device registration and supervision and inspection, establishment of medical device adverse event monitoring system, and carry out monitoring and disposal work; responsible for the development of medical devices Supervise and manage the inspection system and organize the implementation, and organize investigation and punishment of major illegal acts. Establish a problem product recall and disposal system and supervise implementation.

The State Food and Drug Administration is in charge of the supervision and administration of medical equipment throughout the country. The food and drug supervision and administration department of the local people's government at or above the county level is responsible for the supervision and administration of medical devices in its administrative region.

(2) Industry supervision system

The medical device industry is one of the key national management industries. The National Development and Reform Commission is responsible for implementing the industrial policy of the medical device industry, researching and formulating industry development plans, guiding the adjustment of industry structure and implementing industry management; the Ministry of Health is responsible for formulating the strategic objectives, plans and policies for health reform and development, and drafting laws and regulations related to medical devices. The draft, formulate medical device regulations, and formulate relevant standards and technical specifications in accordance with the law; the State Food and Drug Administration is responsible for administrative supervision and technical management of the development, production, circulation and use of medical devices.

China's medical device industry currently implements classified supervision and management. Supervision and management includes supervision of products, product use and supervision of medical device manufacturing enterprises. Supervised products are designed to verify the safety and effectiveness of the product. Supervising production enterprises aims to ensure that product quality is stable, safe and effective, and is reflected in the audit of the quality management system of manufacturing enterprises, and regular review. China reviews the quality management system standards for medical devices, and adopts the medical device industry standard YY/T 0287-2003 "Medical Device Quality Management System for Regulatory Requirements", which is equivalent to the use of ISO13485 "Medical Device Quality Management System for regulatory requirements." 》.

A. Medical devices are classified and managed according to the degree of risk

1 The first category is medical equipment with low risk level and regular management to ensure its safety and effectiveness; 2 The second category is medical equipment with moderate risk and strict control and management to ensure its safety and effectiveness; It is a medical device that has a high risk and needs special measures to strictly control management to ensure its safety and effectiveness.

B. Medical device implementation of product filing and registration management system

The first type of medical devices are subject to product filing management, and the second and third types of medical devices are subject to product registration management. The food and drug supervision and administration department that accepts the application for registration shall make a decision based on the evaluation opinions of the technical assessment agency. If it meets the requirements for safety and effectiveness, it shall be registered and issued with the Medical Device Registration Certificate.

1 For the record of the first type of medical device products, the filer shall submit the filing materials to the food and drug supervision and administration department of the municipal people's government in the local district; 2 apply for the registration of the second type of medical device products, and the applicant for registration shall go to the local province or autonomous region. The food and drug supervision and administration department of the municipality directly under the Central Government shall submit the application materials for registration; 3 the application for registration of the third category of medical device products, the applicant for registration shall submit the application for registration to the food and drug supervision and administration department of the State Council.

C. Medical device manufacturing enterprises implement filing and production licensing system

1 For the production of the first type of medical devices, the production enterprises shall file with the food and drug supervision and administration department of the municipal people's government where the localities are located; 2 if they are engaged in the production of the second and third types of medical devices, the production enterprises shall go to the local provinces, The food and drug supervision and administration department of the people's government of the autonomous region or municipality directly under the Central Government shall apply for a production license. The food and drug supervision and administration department shall carry out verification in accordance with the requirements of the medical device production quality management norms formulated by the competent department of the industry. For production enterprises that meet the specified conditions, the license is granted and issued to the Medical Device Production License. Enterprises engaged in the production of Class II and Class III medical devices are required to obtain the Medical Device Registration Certificate and the Medical Device Production License.

3 Enterprises exporting medical devices shall ensure that the medical devices they export meet the requirements of the importing country (region). Those engaged in the operation of the second type of medical devices shall be filed by the operating enterprise with the food and drug supervision and administration department of the municipal people's government where the locality is located; if the third type of medical device is engaged in operation, the operating enterprise shall provide food to the municipal people's government of the district. The drug regulatory authority applied for a business license and was approved and obtained the Medical Device Business Enterprise License.

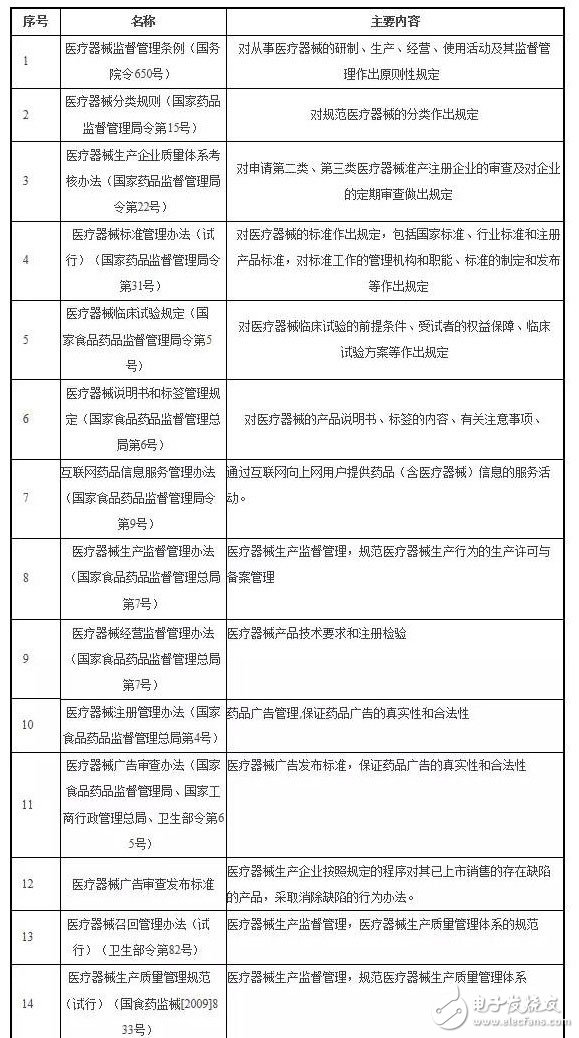

2. The main laws, regulations and policies involved in the company's industry are as follows:

V. Favorable factors and unfavorable factors affecting the development of the industry

(1) Favorable factors

1. Strong support from national policies

Since 2014, the relevant state regulatory authorities have taken active measures to create a good development environment for the medical device industry: In 2014, the State Food and Drug Administration carried out a five-month “five rectification†special action, focusing on rectification. Five kinds of behaviors such as false registration of medical devices, illegal production, illegal operation, exaggeration of publicity, and use of unlicensed products have effectively regulated the market and contributed to the healthy development of the medical device industry. In March 2015, the Ministry of Science and Technology issued the digital diagnosis and treatment. The special equipment implementation plan (draft for comments), from 2015 to 2020, the main tasks of the development of the medical device industry are major equipment R&D, cutting-edge and common technology innovation, application solution research, application demonstration and evaluation research. After the “Twelfth Five-Year Plan†period of promotion and localization of industrial policy guidance and preparation, China will further increase the policy and investment of the digital diagnosis and treatment equipment industry in the future. During the “13th Five-Year Plan†period, the digital diagnosis and treatment equipment industry will achieve breakthroughs. Harvest, the future domestic digital diagnosis and treatment equipment will continue to develop at a high speed.

The national medium- and long-term development plan regards the medical device industry as a key development area. The 2006 National Medium- and Long-Term Science and Technology Development Plan was first written into the development of the medical device industry. With the strengthening of the country's economic strength, various types of research or development-funded projects (such as the 863 Program, national key projects, industrialization projects, etc.) have significantly increased the number of topics related to the inclusion of medical materials and products. The country's huge investment in scientific research and development in the field of medical materials and products has greatly improved the technical level of the industry and shortened the product renewal cycle.

In 2011, the Ministry of Science and Technology released the “Special Plan for the Twelfth Five-Year Plan for Medical Device Technology Industryâ€, which will “break through a number of common key technologies and core components, and focus on the development of a number of independent intellectual property rights, high performance, high quality and low The cost and the basic medical device products that rely mainly on imports to meet the needs of China's primary health care system construction and clinical routine diagnosis and treatment are included in the overall goal of China's medical device development. In 2006, the State Council issued the National Medium- and Long-Term Science and Technology Development Plan ( 2006-2020) As a guiding document for the development of science and technology, we will incorporate “the breakthrough in key medical devices and the technological capabilities for industrial development†into the development goals, and move the focus of disease prevention and control, adhere to prevention, promote health and prevent and treat diseases. Combining, researching key technologies for prevention and early diagnosis, significantly improving the ability to diagnose and prevent major diseases, developing advanced medical equipment, and promoting independent innovation of medical devices, incorporates development ideas and requires “focus on the development of new types of treatment and routine diagnosis and treatment equipmentâ€.

2, the medical device market has broad prospects

The medical device industry applies a large number of new technologies and materials, involving the interdisciplinary integration of optical, electronic, ultrasonic, magnetic, isotope, computer and other disciplines, including artificial materials, artificial organs, biomechanics, monitoring instruments, diagnostic equipment, imaging technology, Information processing, image reconstruction and other technologies are the first to be applied in medical device products.

3. The downstream market has broad prospects

With the introduction of the “Deepening the Medical and Health System Reform Plan and Implementation Plan during the Twelfth Five-Year Planâ€, the new medical system reform plan further emphasizes the public welfare nature of the medical and health undertakings, and strives to accelerate the improvement of the universal medical insurance system, consolidate and improve the basic drug system and the grassroots level. The medical and health institutions operate a new mechanism, actively promote the reform of public hospitals, and coordinate the improvement of basic public health services, medical and health resources allocation, social capital medical treatment, medical and health informationization, pharmaceutical production and circulation, and medical and health supervision systems. reform. According to the “Main Work Arrangement for Deepening the Medical and Health System Reform in 2013â€, the current basic medical insurance for urban employees, basic medical insurance for urban residents and new rural cooperative medical care cover the three basic medical insurance participation rates of all urban and rural residents. the above. The company's end customers belong to the industry at all levels of hospitals, community or rural health service stations, local disease control centers and other health care services. With the advancement of the medical system reform, the development of China's economy and the aging of the country, the improvement and improvement of the downstream industry customers will provide the company with more market space.

(2) Unfavorable factors

1. Competition of foreign companies

At present, it is the major medical equipment companies in foreign countries such as GM and Philips that fully grasp the key bio- and new-material industrialization technologies. They have the advantages of complete industrial chain from upstream material research and development to downstream industrial application. In recent years, China's catch-up speed in this field has been accelerating, but at present, there is no enterprise in China that has the ability to fully grasp the control of upstream materials research and development, and maintain upgrades and innovations synchronized with the international. In addition, domestic companies have significant gaps with foreign manufacturers in terms of capital capabilities and brand influence.

2. The threat of new entry into the enterprise

The higher gross profit margin of medical device products and huge market growth space will attract more domestic and foreign manufacturers to enter the industry, especially large enterprises with strong strength, which can be compared with domestic market by virtue of their mature market experience and capital advantages. Public company manufacturing companies conduct mergers and acquisitions, thereby occupying or expanding their market share in the domestic medical device industry and increasing the intensity of market competition. In order to maintain the leading position of its industry, existing manufacturers in the industry must increase investment in research and development, enhance their independent innovation capabilities, continuously introduce new products, improve product lines, and expand financing channels. Through capitalized and market-oriented standardized operations, they can guarantee their The dominant position in the market competition.

3, the product added value is low, the competition is fierce

Although low value-added products have a certain international market share, they have little contribution to the development of the industry. Many companies have become "manufacturing centers" in overseas markets, earning low manufacturing costs. In addition, the cost of domestic labor is increasing in recent years, and the operating costs of medical device companies are rising. This has brought severe challenges to the survival and development of many small and medium-sized enterprises. As the industry continues to regulate, some small and medium-sized medical device companies are facing the risk of being eliminated. In the international market, Chinese medical device companies have already faced the situation that China's manufacturing low-cost advantage has gradually weakened or even disappeared; in the domestic market, the result of low cost and low price is fierce market competition, and the cost advantage of large-scale enterprises is gradually reflected. Many SMEs face problems of survival and development.

4. Insufficient research and development capabilities and weak innovation capabilities

At present, most medical device manufacturers in China lack technological innovation ability, poor research equipment and basic conditions, insufficient research and development investment, and weak ability to transform scientific and technological achievements. In the field of high-end medical equipment, there is no technology and strength to surpass multinational enterprises and domestic mainstream. Enterprises can only take the road of imitation and fight the price war.

Zhejiang Baishili Battery Technology Service Co,.Ltd. , https://www.bslbatteryservice.com